SEASONED TRADELINES boost credit scores fast. Seasoned Tradelines also build up your credit history FAST.

Some things Our Seasoned Tradelines have been used to Qualify for:

Loans, High Limit Credit Cards, Refinancing, BMW, Cadillac, Mercedes, Lamborghini

What Are Seasoned Tradelines?

Seasoned Tradelines are credit tradelines that are at least 1-2 yrs of age.

A Seasoned tradeline boost credit scores fast. Seasoned Tradelines also build up your credit history.

The basic premise is that the tradeline (or “account”) is seasoned (or “aged”) so that when you’re added to it as an authorized user, your credit score is positively affected.

How Do Seasoned Tradelines Work?

A Seasoned tradeline can be used to increase your average age of accounts and this is a major factor in credit scoring. A seasoned tradeline may also decrease your debt-to-credit ratio, due to the fact older cards usually have higher limits than new cards.. These benefits result in an increased credit score and more credit approvals at good rates.

- There are many credit scoring models, but there’s only one that dominates the credit scoring market — It is the FICO credit score. According to myFICO.com, the FICO score developer, “90 percent of financial institutions in the U.S. use FICO scores in their decision-making process.”

FICO scores only range from 300 to 850, a higher number indicates lower risk.

A consumer only has three FICO scores, one provided by the three major credit bureaus: Experian, Equifax and TransUnion.

What goes into your credit score?

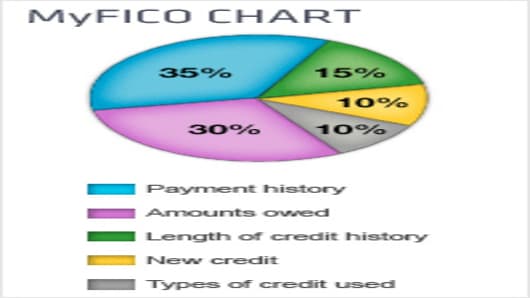

Information from your credit reports go into five categories that make up your FICO credit score. The credit scoring model consider some factors more than others, such as debt owed and payment history.

- Payment history: (35 percent) — payment information, including public records. and any delinquencies

- Amounts owed: (30 percent) — How much you owe on your accounts. The amount of available credit you’re using on revolving accounts is heavily weighted.

- Length of credit history: (15 percent) — How long ago you opened your accounts.

- Types of credit used: (10 percent) — The mix of accounts you have, like installment and revolving.

- New credit: (10 percent) — new credit applications, including recently opened accounts and credit inquiries.

Information such as age, marital status, income, employment, race and address don’t affect the score.